Paving the way to payments modernization with a Shared Hierarchical Ledger System

A few days ago, the Secretary of the U.S. Treasury admitted that she’s still on the fence about digital currency. Unlike the Bitcoin-loving president of El Salvador, Secretary Yellen thinks further study is warranted before diving headfirst into the digital currency deep end.

This hesitancy is good. It’s worth asking a few questions: What’s so great about digital currency? What will it allow us to do that we can’t already do within our current two-tier monetary system?

The answers to these questions are multifaceted and can depend largely on where you are since the drivers to adopt digital currency differ from one country to the next. Sweden, for example, is virtually cashless. The Swedish central bank is responsible for issuing money to citizens, and if it can’t do so because people don’t use cash, then a different form of currency makes sense. If we look at developing countries, financial inclusion becomes more of a driver for adopting digital money. And of course, from a corporate treasury perspective, the speed of settlement, reduced costs, and the potential for conditional payments enabling new payment models are all very enticing.

Adopting central bank digital currency (CBDC) doesn’t have to be the first step to realizing the benefits of digital currency, however. In fact, individuals can have universal access to instant, cheap, and safe payments without CBDC. Other drivers, such as preventing currency substitution, maintaining (or establishing) currency hegemony, and improving payments between countries, can also be addressed without wholesale adoption of CBDC.

The key is payments modernization. Real-time payments, account-to-account payments, and open APIs are all great examples. But payments modernization can also be viewed as the first step toward the adoption of CBDC. If done correctly, it can create a framework to facilitate the interconnection of tokenized central bank money and commercial bank money, much in the same way that money works today. It just needs to be more efficient and totally secure.

I’m a payments nerd, not a crypto fanatic. But I do believe that blockchain holds the answer to payments modernization and the creation of a Regulated Liabilities Network (RLN). Yet, in order to maintain the current two-tier monetary system, dispersed ledger technology must preserve the relationship between central banks and commercial banks.

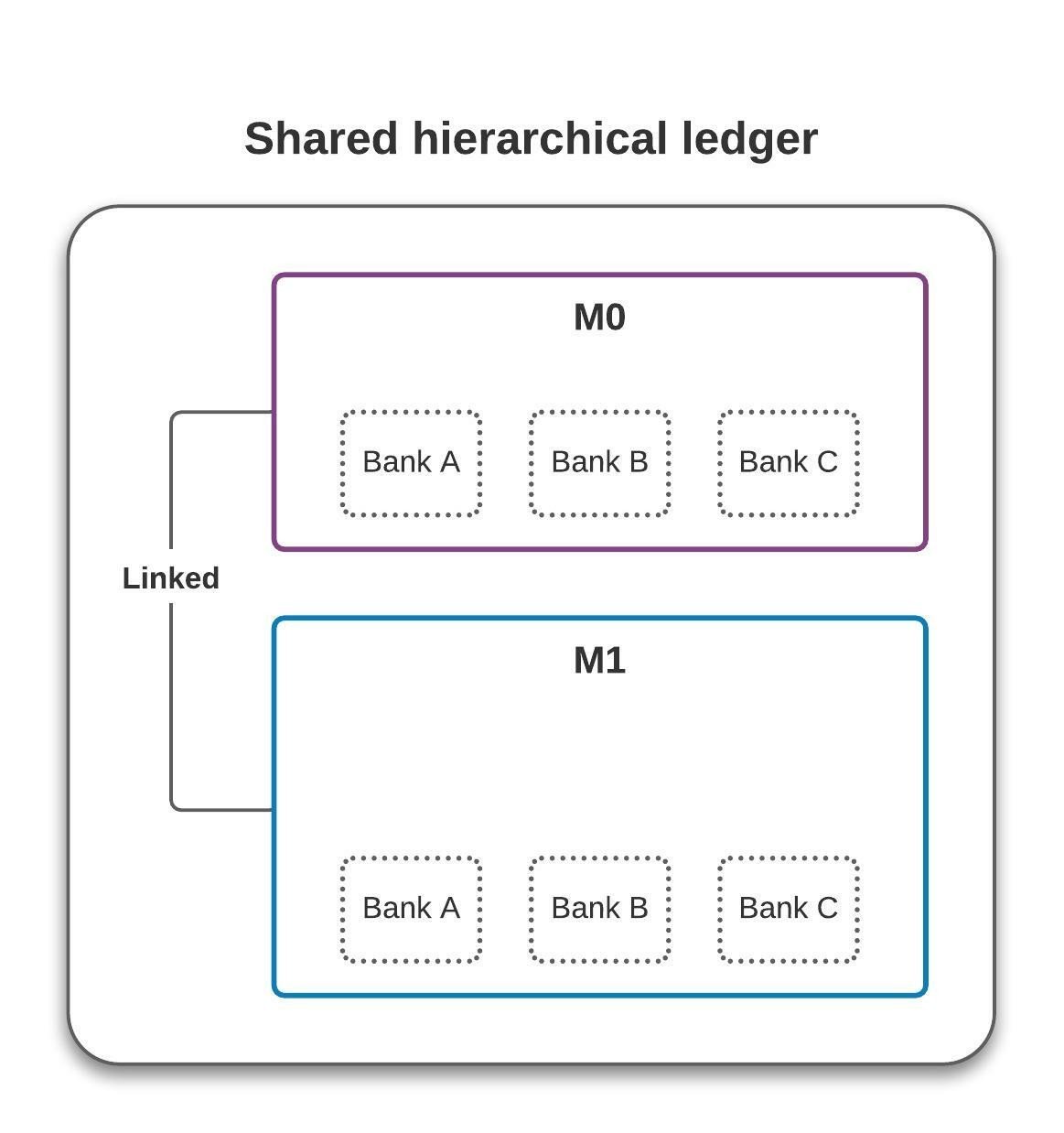

A shared hierarchical ledger could create this type of RLN system that enables the tokenization of both central bank money and commercial bank money. The central bank portion of the ledger would be designated M0, and the commercial bank portion of the ledger, M1. M0 and M1 are distinct but joined in a hierarchical fashion.

This shared hierarchical ledger framework enables instant settlement between banks and their customers on the network. Domestically, it includes payments between individuals (P2P), between businesses (B2B), and from individuals to businesses (C2B). Payments are always “push payments” (credit transfers) and can be pre-authorized to create pull-like (debit transfer) payments.

In the case of cross-border payments, a shared hierarchical ledger would allow banks to avoid routing payments through multiple intermediaries. Instead, a hierarchical ledger would allow instant, low-cost point-to-point transactions with currency ledgers that are interconnected through an FX service. The FX service would simply require accounts on the source and destination ledgers of a transaction and provide liquidity to the transacting counterparties.

And this is just the beginning. A shared hierarchical ledger recognizes that banks are already regulated entities. Using the RLN enables banks to do things more efficiently, but from a regulatory perspective, the banks are doing what they already do today: accepting deposits, providing loans, enabling payments, providing trade financing, disbursements, remittances, and merchant payment processing. There’s no need to change national laws or to apply additional regulatory oversight. Banks would remain responsible for KYC when onboarding new customers and AML and sanction screening when processing payments.

An RLN based on a shared hierarchical ledger would also be highly cost-effective. If shared ledgers are connected through a single cloud-based platform, banks will benefit from economies of scale. Furthermore, the reduced reliance on correspondent banking provides additional savings, as does the ability to lower liquidity requirements, since banks can move assets instantly to where they are needed.

A modern RLN based on a shared hierarchical ledger would also use state-of-the-art authentication, tokenization, access management, and other tools which are generally not available to your average commercial bank, making the network highly secure. And perhaps most importantly, payment modernization based on a shared hierarchical ledger system can be realized in a matter of weeks or months, instead of years or even decades. This point is critical to stave off the threat of an unregulated internet of value.

At M10, we encourage central banks to continue researching and experimenting with CBDC. We also encourage implementing payments modernization solutions in parallel to connect M1 and M0 and provide future options for CBDC. This two-pronged approach is already bringing the key benefits of CBDC to market faster and has the potential to dramatically reduce the cost to central banks.